On Knowing Nothing Different

Mike Earl, CFP®, CPWA®

Mike Earl, CFP®, CPWA®

Growing up, I was always intrigued by money. I liked earning it, and I really liked saving it.

In May 1997, about a month shy of my 14th birthday, I biked from our family’s home in Eden Prairie over to the Chanhassen McDonald’s – a grueling one-mile ride (uphill both ways). I went with a friend from the neighborhood. We both applied for jobs there on the spot, and I remember nervously wondering if they had any interest in hiring me.

Lo and behold, I got the job. You can imagine the rigorous hiring standards for young teenagers at McDonald’s. The starting pay was $5.50/hour. The next question was: what do I do with all this money I’m earning?

Growing up, my dad had taught me a really simple method for managing my money:

GIVE 10% TO GOD/CHARITY.

SAVE 10% FOR YOUR FUTURE.

SPEND THE REMAINING 80%.

I remember thinking to myself, “why on earth would I spend 80% of what I make?! I don’t need all that spending money.”

We all benchmark to something in making financial decisions. For example, many people simply contribute enough to their 401(k) to earn the full company match. This is why a typical contribution rate to a 401(k) is about 6% of one’s pay. But why not save double, triple, or even more of what is required to get the full company match?

Or with vehicle purchases, the tendency is to benchmark to what other people in our neighborhood are doing. So when we see all the shiny SUVs and trucks in the neighborhood, it seems normal to pay $40,000 or more for a motor carriage.

Back to my story:

I saved about $2,500 from age 14-16, working at McDonald’s. When I turned 16, I did what many do at that age: I bought a car I didn’t actually need. Mom and Dad chipped in to help me buy a 1992 Toyota Corolla for $4,400. And poof, there went 100% of my savings.

So, I had worked for two years in order to obtain a new form of transportation that I didn’t actually need. Sure, someday I would have more of a need for a car, but not at that time. Bikes are a really, really inexpensive form of transport.

In hindsight, my dad could have given me a much more savings-oriented plan – and I would have taken it as gospel. Had he told me to give 10% of my money to God/charity, save 50%, and spend 40%, I would have gone ahead and done it.

Today, my family strives to give away 11-12% of our income, save 18-20% for retirement, set aside a bit of money for our children’s future education, save a bit for future spending (such as for vehicles and vacations), and spend the remainder. It works well.

As my children grow older (my oldest is 4 years old), I will endeavor to give them simple rules for financial success. For instance, here is a potential savings strategy I would give to them:

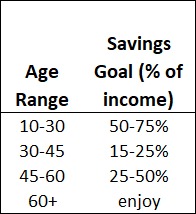

When you are young and providing only for yourself, it should not be too difficult to save 50% or more of your income.

When you start raising a family, your savings rate will naturally go down. But the bar should not be lowered all the way down to a 5% or even 10% savings rate. If you can save 15% or more of your income during your child-rearing years, you will lap your peers many times over.

At some point, your 15-year mortgage will be paid off, and you can crank your savings rate back up significantly. At that point, you’re sprinting toward financial independence.

These percentages are not set in stone; rather, they are meant to give a different kind of benchmark to think about.

If we can change our internal assumptions/beliefs about saving, we can easily secure financial peace for ourselves and our loved ones. If young people are taught growing up that a 15% savings rate is a bare minimum in life, they can make it happen. They’ll know nothing different.

Because The Wealth Group, Austin B. Colby & Associates is independent of Raymond James, the expressed written opinions above are our own and not necessarily reflective of Raymond James’ opinions.