Your Million Dollar Opportunity

By: Mike Earl, CFP®, CPWA®

If you want to make personal finance as simple as possible, you could boil it down to two crucial areas: housing and transportation. As we have written about in the past, these two categories of spending constitute the lion’s share of the average American family’s spending (and rightly so). These two categories account for 43.5% of after-tax spending for the average American household.

As our friend and fellow financial planner Ben Carlson writes, “If you can right-size your housing and transportation costs on a monthly basis, everything else becomes easier from a saving and budgeting perspective.”

Vehicles are like clothing: they serve a crucial purpose in our lives, but they will ultimately be worthless. When it comes to depreciating assets, the goal is to minimize the damage they can wreak on your financial life. Now, if you are a financially independent multi-millionaire, then go to town on that Maserati! But for most folks, the name of the game is keeping vehicle purchases modest -- particularly in the "accumulation phase" of your investing life.

Vehicles end up being a part of our lives for many decades. If a man buys his first car at age 22 and his last car at 82, that’s a lot of vehicle transactions over a 60-year period.

As of year-end 2017, more than 108 million Americans had a car loan. That’s about 44% of American adults.

The average new car loan amount for 2017 was over $31,000.

85% of new vehicle purchases are made on credit.

As of January 2018, the average new car purchase price in America was $36,270.

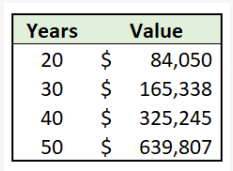

What if that average purchase price was knocked down to $15,000? And what if the $21,270 difference was invested in a long-term investment portfolio that averages a 7% rate of return? Here is what the value of that $21,720 would grow to in 20, 30, 40, and 50 years:

The power of compounding (and opportunity cost) at work. Will the person in the $15,000 vehicle be any worse-off in life vs. the person in the $36,270 vehicle? Not in any meaningful sense. We have already demonstrated the fancy cars you can buy for less than $15,000.

As humans, we have infinite desires but finite resources. We all must find a middle zone between our desires and resources. Driving a $15,000 vehicle is not much of a sacrifice of our desires.

It’s one thing to talk in the abstract about “the power of compounding.” But it gets really practical when making decisions about housing and vehicles. If you want compounding to work for you – not against you – then start with thoughtful decisions about the home and vehicle you buy.

The table above illustrates the difference in wealth accumulation based on one single vehicle purchase. Think about the extraordinary effects of a married couple right-sizing their vehicle purchases over a lifetime? It’s easy to see that we are talking about millions of dollars of wealth difference, assuming the vehicle cost savings are invested for long-term growth.

Lastly, take a look at this chart assembled by Ben Carlson. This table is derived from U.S. News & World Report’s list of the 15 “best” SUVs for 2018:

SUVs have gotten really expensive. The average monthly payment there is $766 (assuming middle of the MSRP range for purchases). If you invest $766 per month in an investment portfolio earning 7%, you have $1,379,608 after 35 years.

What does this mean to you, our client?

Think thoughtfully about your vehicle purchases. Talk to us about how vehicle purchases will impact your net worth over time (and subsequently, your date of reaching Financial Independence). Understand the trade-offs we all make in life: a nice vehicle today likely means working longer and harder on the back-end.

Sources:

2) https://www.finder.com/car-loan-statistics

4) http://awealthofcommonsense.com/2018/07/are-suvs-ruining-retirement-savings/

5) https://www.statista.com/statistics/453000/share-of-new-vehicles-with-financing-usa/

Because The Wealth Group, Austin B. Colby & Associates is independent of Raymond James, the expressed written opinions above are our own and not necessarily reflective of Raymond James’ opinions.