The Big Picture

By: Mike Earl

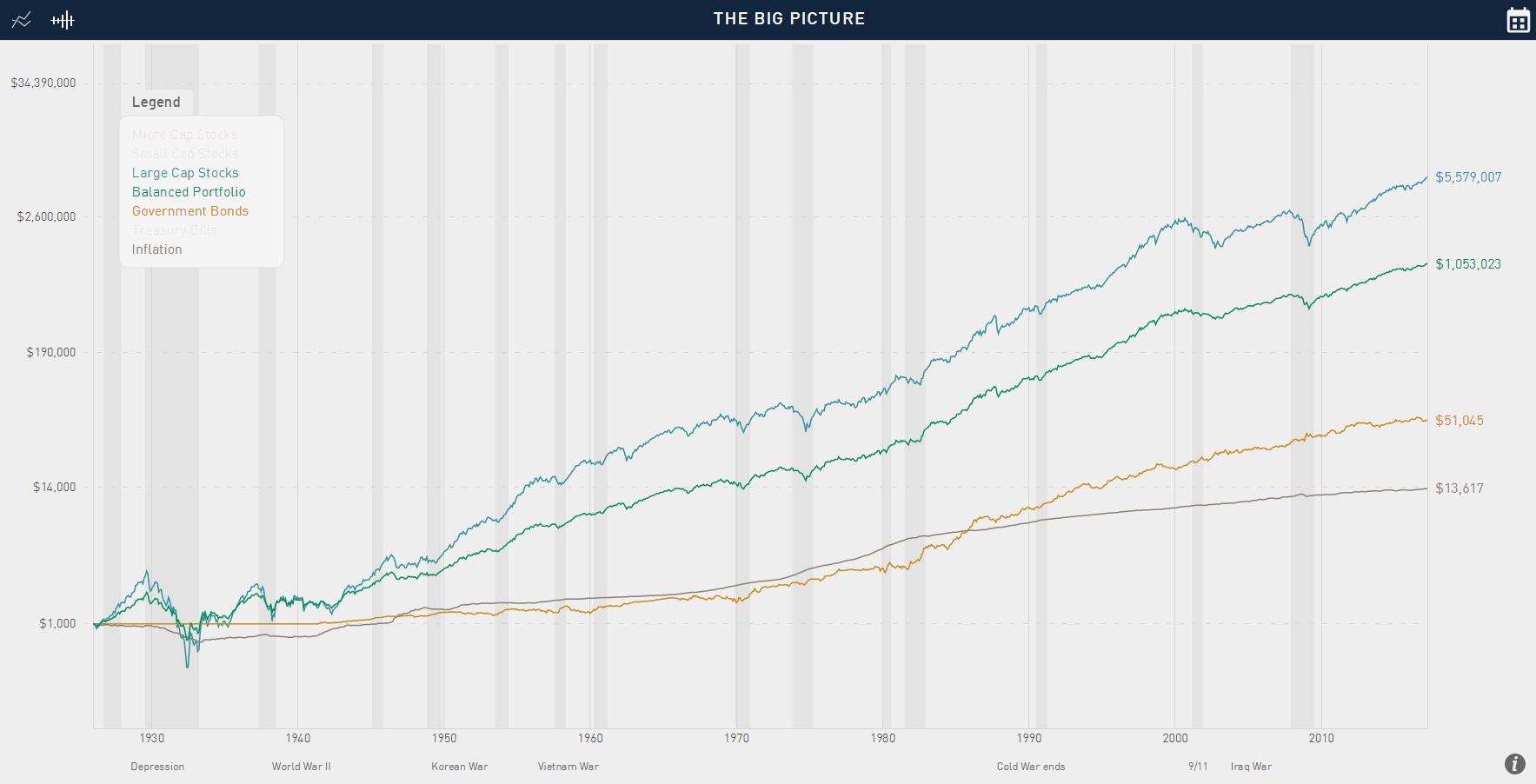

Owning stocks is not always a pleasant experience. The Great Recession of 2007-2009 ultimately cut US stocks by more than 54%. The Great Depression brought nearly a 90% reduction in US stocks. Those drawdowns are Exhibit A of why our clients in distribution mode (i.e. Retirement) never own 100% stocks. In fact, they typically own anywhere from 45% - 65% in their portfolio in stocks, with the reminder invested in a diversified portfolio of bonds and some cash. That way, the nasty shocks that inevitably hit equity markets will be cushioned by the bond and cash exposures.

But in spite of the six bear markets the US has experienced since the 1920s, a $1,000 investment into large company US stocks in 1926 would have been worth more than $5,500,000 at the end of 2016. It's breathtaking, once you stop to think about it.

When you have a 91-year perspective, the case for stocks is crystal-clear. But none of us live with 91-year timelines. Not only that, but humans are wired to experience much more pain from losing money than gaining money (at a 2.5x ratio, in fact). So we remember the Tech Bust and the Great Recession viscerally.

While the case for stock investing should be an easy one to make, Millennials (born 1980-1994)

have become notorious for being massively under-invested in stocks:

The wealth-building power of owning stocks is undeniable (just ask Warren Buffett). Yet young Americans today own significantly less stocks within their investment portfolios than older Americans.

This chart explains one of the reasons we are so passionate about working with younger clients. While young people today have unlimited information at their fingertips, that information makes it harder than ever to know which information to trust. Many Millennials don't trust the stock market, after watching two large crashes in the span of 10 years.

The storms will come again in equity markets. Corrections (10% decline or more) happen about once per year. Only 1 in 5 of those corrections turn into bear markets (20% decline or more). We don't know when they're going to happen, but we can be mentally prepared to know they will come.

Source: University of Chicago